Juggling a 403(b) and a Solo 401(k)? You’re not alone! Many professionals today have a mix of W-2 and 1099 income, making retirement planning a bit more complex. But don’t worry, with the right strategy, you can maximize your tax-advantaged savings and build a comfortable nest egg.

At XOA TAX, we understand the unique challenges and opportunities that come with managing multiple income streams. This blog post will guide you through key considerations for dual-income professionals like yourself, focusing on how to leverage both your 403(b) and Solo 401(k) effectively.

Key Takeaways

- Contribution Limits: Understand the combined limits across all your retirement accounts.

- Tax Implications: Explore the distinct tax benefits of 403(b)s and Solo 401(k)s.

- QBI Deduction: Learn how your retirement contributions can impact this valuable deduction.

- Investment Choices: Compare the options available in each plan type.

- Strategic Planning: Develop a personalized strategy to maximize your retirement savings.

Understanding Contribution Limits Across Multiple Retirement Accounts

The IRS sets annual limits on how much you can contribute to retirement accounts. For 2024, the employee contribution limit for both 403(b) and 401(k) plans is $23,000, or $30,500 if you’re 50 or older (including the $7,500 catch-up contribution). This limit applies collectively to all your 403(b) and 401(k) accounts. So, if you contribute to both a 403(b) through your employer and a Solo 401(k) for your self-employment income, your combined employee contributions cannot exceed this limit.

However, with a Solo 401(k), you can also make employer contributions, which are not subject to the same limit as employee contributions. For 2024, the total combined contribution limit (including both employee and employer contributions) for a Solo 401(k) is $69,000, or $76,500 if you’re 50 or older (including the catch-up contribution). This allows you to potentially shelter a significant portion of your self-employment income. It’s important to note that employer contributions to a Solo 401(k) are limited to the lesser of 25% of your compensation or 20% of your net adjusted self-employed income (after deducting self-employment tax).

Tax Implications of 403(b) vs. Solo 401(k) Contributions

Both 403(b)s and Solo 401(k)s offer significant tax advantages, but they differ in key ways:

- 403(b): Contributions to a traditional 403(b) are typically made pre-tax, reducing your taxable income now. Some employers may offer matching contributions, which is essentially free money! Be sure to check with your employer to understand their specific matching policy. Not all 403(b) plans offer Roth options, so be sure to inquire about your plan’s specific provisions.

- Solo 401(k): A Solo 401(k) offers more flexibility, allowing you to contribute both as an “employee” (up to the annual limit) and an “employer” (up to 25% of your net adjusted self-employed income).

Impact on Qualified Business Income (QBI) Deduction

The Qualified Business Income (QBI) deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income. Your QBI is calculated by subtracting your business expenses from your business revenue. It’s important to understand that contributions to your Solo 401(k) reduce your QBI. This is because the QBI deduction is calculated based on your net business income after deducting retirement plan contributions.

Example: Let’s say your QBI is $100,000, and you contribute $20,000 to your Solo 401(k). This reduces your QBI to $80,000 for the QBI deduction calculation.

Strategically allocating contributions between your 403(b) and Solo 401(k) can help you optimize your QBI deduction while still maximizing your retirement savings. Keep in mind that certain high-income thresholds can affect the QBI deduction, with phase-out rules applying to those with higher incomes.

Evaluating Investment Options and Fees

- Investment Choices: Solo 401(k)s often provide a wider range of investment options compared to employer-sponsored 403(b) plans. You might have access to individual stocks, bonds, mutual funds, and even alternative investments.

- Fees: Pay close attention to fees in both plans. Some 403(b) plans may have higher administrative fees or limited investment choices, which can impact overall returns. Conversely, Solo 401(k) plans, especially those established with low-cost providers, can offer more flexibility and potentially lower fees. Websites like 403bcompare.com can help you evaluate your plan options and compare fees.

Strategic Recommendations

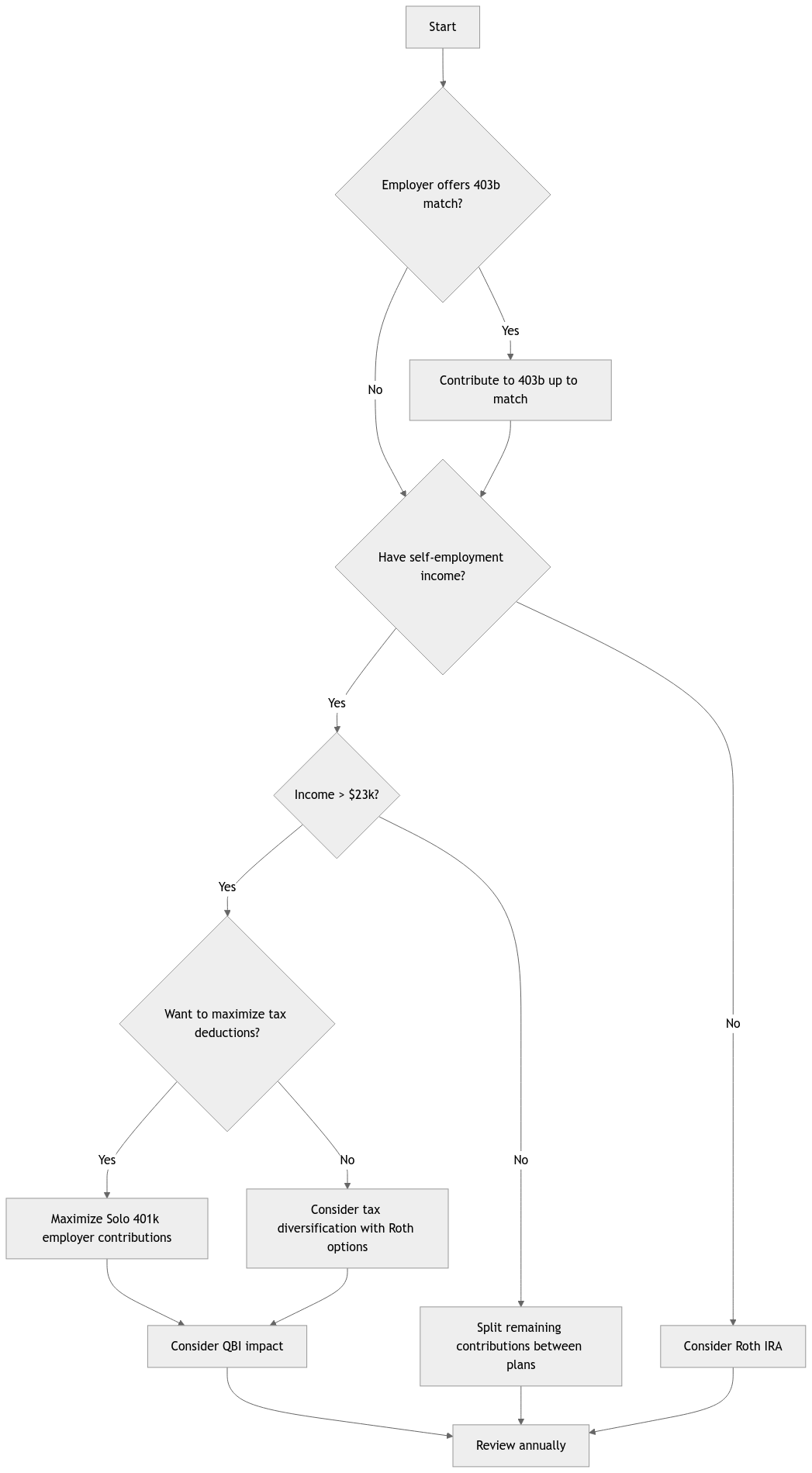

- Maximize Employer Match: If your employer offers a 403(b) match, contribute enough to get the full match. It’s a guaranteed return on your investment!

- Solo 401(k) for Self-Employment Income: Leverage your Solo 401(k) to shelter more of your self-employment income, keeping in mind the contribution limits for both employee and employer contributions.

- Consider Your QBI: Factor in the potential impact on your QBI deduction when deciding how much to contribute to each plan.

- Diversify Your Investments: Don’t put all your eggs in one basket! Spread your investments across different asset classes to reduce risk.

- Explore Roth Options: A Roth IRA can be a valuable addition to your retirement plan, offering tax-free growth and withdrawals in retirement.

Important Deadlines and Considerations

- Solo 401(k) Deadline: To establish a Solo 401(k) for the current tax year, you generally need to do so by September 30th of that year.

- Form 5500-EZ: If your Solo 401(k) has over $250,000 in assets, you’ll need to file Form 5500-EZ annually. You can find instructions and the form itself on the IRS website.

403(b) vs Solo 401(k) Comparison (2024)

| Feature | 403(b) | Solo 401(k) |

|---|---|---|

| Contribution Limits | ||

| Employee Contribution | $23,000 | $23,000 |

| Catch-up (50+) | $7,500 | $7,500 |

| Total Limit | $69,000 | $69,000 |

| Plan Features | ||

| Investment Options | Limited by plan | Wide range |

| Roth Option | Plan dependent | Available |

| Loans | Plan dependent | Available |

| Key Deadlines | ||

| Plan Setup | N/A | September 30 |

| Employee Contributions | December 31 | December 31 |

| Employer Contributions | December 31 | Tax filing deadline |

| Form 5500-EZ | N/A | Required if >$250k |

| Tax Considerations | ||

| Pre-tax Contributions | Yes | Yes |

| QBI Impact | No impact | Reduces QBI |

| State Tax Treatment | Varies by state | Varies by state |

Understanding the SECURE 2.0 Act

The SECURE 2.0 Act of 2022 brought about significant changes to retirement savings rules. While many provisions are still being implemented, it’s crucial to stay informed about how these changes might affect your retirement planning. Some key aspects of SECURE 2.0 include:

- Increased Catch-Up Contributions: Starting in 2025, catch-up contribution limits will increase for individuals aged 60-63.

- Required Minimum Distributions (RMDs): The age for taking RMDs has increased, allowing your retirement savings to grow tax-deferred for longer.

- Roth Options for Employer Matches: SECURE 2.0 allows employers to offer Roth matching contributions, giving you more flexibility in how your retirement savings are taxed.

We’ll continue to provide updates and guidance on the SECURE 2.0 Act as new provisions are implemented.

Required Minimum Distributions (RMDs)

RMDs are the minimum amounts you must withdraw from your retirement accounts each year once you reach a certain age. The SECURE 2.0 Act has increased the age for taking RMDs. Currently, for those who turned 73 in 2023, the RMD age is 73. This will increase to age 75 by 2033. Understanding RMD rules is crucial to avoid penalties and optimize your retirement income.

Loan Provisions: 403(b) vs. Solo 401(k)

Both 403(b) and Solo 401(k) plans may allow you to take loans from your account balance. However, the specific rules and limitations can vary. It’s important to compare loan provisions carefully before making any decisions. Generally, Solo 401(k)s offer more flexibility when it comes to loans, but it’s crucial to understand the repayment terms and potential consequences of defaulting on a loan.

FAQs

Can I contribute to both a 403(b) and a Solo 401(k) in the same year?

Absolutely! You can contribute to both, but remember the combined employee contribution limit for 2024 is $23,000 (or $30,500 if you’re 50 or older). However, you can make additional employer contributions to your Solo 401(k).

What happens if I overcontribute to my retirement accounts?

You’ll generally need to withdraw the excess contributions and may be subject to penalties. It’s crucial to keep track of your contributions and stay within the limits.

Can I roll over funds from my 403(b) to my Solo 401(k)?

In many cases, yes. However, rollovers can have tax implications, and there may be specific rules or limitations depending on your plan providers. It’s always best to consult with your plan administrators or a tax professional before making any decisions.

Connecting with XOA TAX

Navigating the complexities of retirement planning with multiple income streams can be challenging. At XOA TAX, our experienced CPAs can help you develop a personalized strategy to maximize your savings and minimize your tax liability. We can provide guidance on contribution limits, investment options, and the QBI deduction, ensuring you make informed decisions for your financial future.

Contact us today for a consultation:

Website: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/

Phone: +1 (714) 594-6986

Email: [email protected]

Contact Page: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/contact-us/

Disclaimer: This post is for informational purposes only and does not provide legal, tax, or financial advice. Laws, regulations, and tax rates can change frequently, and vary significantly by state and locality. This communication is not intended to be a solicitation and XOA TAX does not provide legal advice. Please consult a professional advisor for advice specific to your situation.