Starting a private practice as a therapist is an exciting journey, filled with the rewards of helping others and building your own business. However, it’s important to be prepared for the financial responsibilities that come with being self-employed, especially when it comes to taxes. This guide will walk you through understanding your tax obligations as a 1099 therapist and provide practical strategies for managing your liability.

Key Takeaways

- Independent therapists are responsible for self-employment and income taxes.

- Accurate record-keeping is essential for managing tax liability and maximizing deductions.

- Estimated tax payments can help avoid penalties.

- Consulting a tax professional can provide personalized guidance.

Understanding Your Tax Obligations

As a 1099 therapist, you’re considered an independent contractor. This means you’re responsible for paying self-employment taxes in addition to regular federal and state income taxes. Let’s break down each type:

1. Self-Employment Tax

This tax covers Social Security and Medicare. It’s calculated at a rate of 15.3% of your net earnings. For 2024, the Social Security portion only applies to the first $168,600 of your earnings.

2. Federal Income Tax

Your federal income tax rate depends on your filing status (single, married, etc.) and your taxable income, which is your income after deductions. The U.S. has a progressive tax system, meaning the higher your income, the higher the tax rate.

You can find further details on the IRS website.

3. State Income Tax

State income tax rates and rules vary significantly. Some states have no income tax, while others have a flat tax rate or a progressive system like the federal government. It’s essential to understand the specific tax laws in your state.

Estimating Your Tax Liability

Estimating your tax liability requires understanding your net income and the applicable tax rates. Here’s a breakdown:

- Calculate Net Income: Start with your gross earnings and subtract any business expenses (we’ll cover common deductions later in this post). For example, if your monthly earnings range from $2,500 to $4,000 and you have a 30% fee to the practice group, your estimated annual net income falls between $21,000 and $33,600.

- Self-Employment Tax: Calculate 15.3% of your estimated net income. This gives you a starting point for your self-employment tax obligation. Remember to factor in the Social Security wage base limit.

- Federal Income Tax: Refer to the Federal Income Tax Brackets table to determine the rate for your income level. Remember that deductions can lower your taxable income, potentially placing you in a lower tax bracket.

- State Income Tax: Research your state’s income tax rates and regulations. Use your estimated net income to calculate your potential state tax liability.

Example: Let’s say your net income is $28,000 after deductions, and you live in California with a 5% income tax rate (for this income level).

- Self-Employment Tax: $28,000 x 15.3% = $4,284 (before the self-employment tax deduction)

- State Income Tax: $28,000 x 5% = $1,400

- Federal Income Tax: This will depend on your deductions and where you fall within the federal tax brackets. Let’s assume your deductions bring your taxable income down to $20,000, and based on the federal tax brackets for single filers, your estimated federal income tax is $1,800.

Recommended Savings Rate

A general rule of thumb is to set aside at least 25% to 30% of your net income for taxes. This provides a cushion to cover federal, state, and self-employment taxes. However, this is a minimum, and your specific savings rate may need to be higher depending on several factors:

- State of Residence: Higher state income tax rates will require a higher savings rate.

- Total Income Level: As your income increases, you may move into higher tax brackets, necessitating a larger savings buffer.

- Deductions and Credits: The more deductions and credits you qualify for, the lower your overall tax liability may be, potentially allowing for a slightly lower savings rate.

It’s crucial to remember that this savings rate is intended to cover all your tax liabilities, including federal, state, and self-employment taxes.

Tips for Managing Your Tax Liability

- Maintain Meticulous Records: Accurate records of all income and expenses are vital. This not only helps you calculate your tax liability correctly but also allows you to maximize deductions. Consider using accounting software or hiring a bookkeeper to streamline this process.

- Make Estimated Tax Payments: As a 1099 therapist, you’re likely required to make estimated tax payments quarterly to the IRS and your state tax authority. This helps avoid penalties for underpayment. You can calculate and pay estimated taxes online or through mail.

- Maximize Deductions: Several deductions are available to self-employed individuals. Common deductions for therapists include:

- Continuing education expenses

- Professional liability insurance

- Office supplies

- Home office expenses (if you have a dedicated workspace)

- Professional association dues

- Electronic health records (EHR) software

- Professional supervision costs

- Business insurance (malpractice, general liability)

- Marketing expenses (website, advertising)

- Plan for Retirement: Contributing to a retirement plan like a SEP IRA or Solo 401(k) can not only help you save for the future but also reduce your current tax liability.

- Health Insurance Deduction: Don’t forget that you can deduct your health insurance premiums as a self-employed individual.

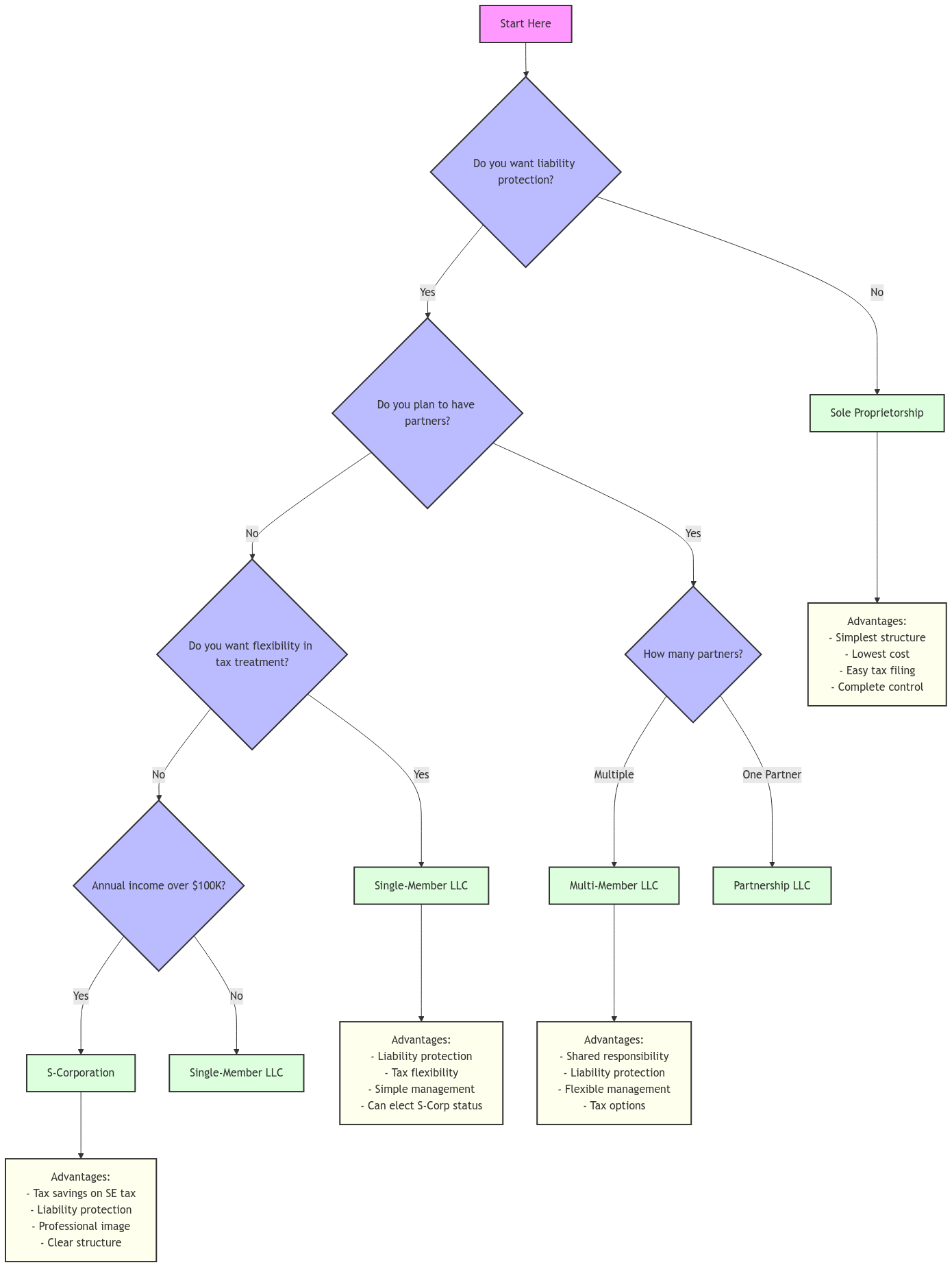

Choosing the Right Business Structure

When establishing your private practice, you’ll need to choose a business structure.

The most common options for therapists are:

- Sole Proprietorship: This is the simplest structure, where you and the business are considered one entity for tax purposes.

- Limited Liability Company (LLC): An LLC offers some personal liability protection and provides flexibility in how you’re taxed. You can choose to be taxed as a sole proprietorship, partnership, or corporation.

Each structure has different tax implications. Consulting with a tax professional or legal advisor can help you determine the best option for your specific needs.

Planning for Retirement

Retirement planning is essential for self-employed individuals. Here are some common retirement plan options for therapists:

- SEP IRA: A Simplified Employee Pension (SEP) IRA allows you to contribute a significant portion of your net earnings, with higher contribution limits than traditional IRAs.

- Solo 401(k): This plan allows you to contribute both as an employee and an employer, offering greater flexibility and potentially higher contribution limits.

Here’s a comprehensive comparison table for SEP IRA and Solo 401(k) plans for the 2024 tax year:

| Feature | SEP IRA | Solo 401(k) |

|---|---|---|

| 2024 Contribution Limits | Up to 25% of net self-employment income, capped at $69,000.

| – Employee Contribution: Up to $23,000; $30,500 if age 50 or older. – Employer Contribution: Up to 25% of compensation. – Total Limit: Combined employee and employer contributions up to $69,000; $76,500 if age 50 or older. |

| Eligibility Requirements | – Self-employed individuals or small business owners. – No age restrictions. – Must cover all eligible employees. | – Self-employed individuals with no employees other than a spouse. – Spouse can participate if employed by the business. – No age restrictions. |

| Tax Advantages | – Contributions are tax-deductible. – Earnings grow tax-deferred. – Distributions taxed as ordinary income. | – Traditional: Same as SEP IRA. – Roth option available for employee contributions. – Loan options may be available. |

| Setup & Administration | – Simple setup with minimal paperwork. – Lower administrative costs. | – More complex setup. – Annual filing requirements (Form 5500) if plan assets exceed $250,000. – Potentially higher administrative costs. |

| Contribution Flexibility | – Employer contributions can vary each year. – No mandatory annual contributions. | – Flexible contribution options, allowing both employee and employer contributions.

|

| Deadline to Establish | Tax filing deadline, including extensions. | December 31 of the year for which contributions are made. |

| Investment Options | Wide range of investment options, including stocks, bonds, and mutual funds. | Wide range of investment options, including stocks, bonds, and mutual funds.

|

| Required Minimum Distributions (RMDs) | Must begin at age 73. | – Must begin at age 73. – Roth contributions are exempt from RMDs. |

| Early Withdrawal Rules | – 10% penalty on withdrawals before age 59½; exceptions may apply. | – 10% penalty on withdrawals before age 59½; exceptions may apply. – Loan options may provide additional flexibility. |

| Best For | – Sole proprietors seeking simplicity. – Those preferring minimal paperwork. – Higher-income earners aiming for substantial contributions. | – Self-employed individuals desiring maximum contribution potential. – Those interested in Roth contribution options. – Individuals who might need to borrow from their retirement funds. |

Note: All contribution limits and ages are for the 2024 tax year and are subject to annual adjustments by the IRS. Consult with a tax professional for advice specific to your situation.

Digital Payment Processing and Taxes

In today’s digital age, many therapists use online platforms like PayPal, Stripe, and Square to process payments. It’s important to understand the tax implications of these services:

- Reporting Requirements: Payment processors typically issue a Form 1099-K if you exceed a certain threshold of transactions or gross payments. This form reports your payment processing income to the IRS.

- Transaction Fees: Be aware of transaction fees charged by payment processors, as these can impact your net income.

- Potential Deductions: You may be able to deduct transaction fees as business expenses.

Telehealth and Tax Considerations

The rise of telehealth has brought about unique tax considerations for therapists providing virtual services:

- Home Office Deduction: If you have a dedicated space in your home used exclusively for telehealth services, you may be eligible for the home office deduction.

- Technology Expenses: You can deduct expenses related to telehealth technology, such as computers, software, and internet services.

- State Regulations: Some states have specific regulations regarding telehealth, which may impact your tax obligations.

Multi-State Tax Considerations

If you practice therapy in multiple states, you’ll need to navigate the complexities of multi-state taxation. This includes:

- Income Allocation: You’ll need to allocate your income to the respective states where you earned it.

- State Tax Returns: You’ll likely need to file separate tax returns in each state where you practice.

- Tax Credits: Some states offer tax credits for telehealth services or other healthcare-related activities.

FAQ Section

Q: What happens if I don’t save enough for taxes?

A: Underpayment can lead to penalties and interest from the IRS and your state. It’s always better to overestimate and adjust as needed.

Q: Can I deduct the cost of therapy sessions for my own mental health?

A: Generally, no. However, if the therapy is related to your work or required for your professional license, it may be deductible. It’s best to consult with a tax professional to determine if your specific situation qualifies.

Q: Are there any tax credits available to therapists?

A: While tax credits vary by state and individual circumstances, some possibilities include the Child Tax Credit or credits for energy-efficient home improvements if you have a home office.

When to Seek Professional Tax Help

While this guide provides a solid foundation for understanding your tax obligations, certain situations warrant seeking professional assistance:

- Complex Tax Situations: If you have multiple income streams, significant investments, or are dealing with a unique tax situation, a tax professional can provide expert guidance.

- Uncertainty About Deductions: If you’re unsure about which deductions you qualify for, a tax professional can help you identify potential savings opportunities.

- Feeling Overwhelmed: Tax preparation can be complex and time-consuming. If you’re feeling overwhelmed, a tax professional can take the burden off your shoulders.

Connecting with XOA TAX

Navigating the complexities of taxes as a 1099 therapist can be challenging. At XOA TAX, we understand the unique needs of independent contractors and can provide personalized guidance to help you minimize your tax liability and achieve your financial goals.

Contact us today for a consultation:

Website: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/

Phone: +1 (714) 594-6986

Email: [email protected]

Contact Page: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/contact-us/

We’re here to help you make sense of your tax obligations and ensure you’re on the right track to financial success.

Disclaimer: This post is for informational purposes only and does not provide legal, tax, or financial advice. Laws, regulations, and tax rates can change often and vary significantly by state and locality. This communication is not intended to be a solicitation, and XOA TAX does not provide legal advice. Please consult a professional advisor for advice specific to your situation.