Ever wonder how some people become super wealthy? It’s not always about winning the lottery or inheriting a fortune. There’s a strategic playbook that many successful people follow, and we’re going to break it down for you, step-by-step. Think of it as your guide to leveling up your finances, inspired by the insights of entrepreneur Alex Hormozi, which you can learn more about in his YouTube video, “How The Ultra Rich REALLY Build Wealth” .

Key Takeaways

- Building wealth requires a combination of earning, saving, and smart investing.

- The ultra-rich focus on long-term strategies and calculated risks.

- Tax-advantaged accounts can play a crucial role in wealth accumulation.

- Seeking professional guidance from qualified experts can optimize your financial decisions.

How the Ultra-Rich Approach Wealth Building

The ultra-wealthy don’t just stash their cash in a savings account. They use a mix of smart strategies to make their money work hard for them. Let’s take a look:

1. Earning More: Laying the Foundation

This might seem obvious, but the ultra-rich prioritize developing valuable skills and pursuing careers with high earning potential. Think of it like building a solid foundation for a house – you need a strong base to support everything else.

For example, imagine someone who takes online courses to learn coding or digital marketing. These in-demand skills can open doors to higher-paying jobs and even entrepreneurial ventures.

2. Passive Investing: Growing Your Wealth Over Time

Imagine your money potentially growing while you sleep! That’s the potential of passive investing. The ultra-rich invest in assets like stocks, bonds, and real estate, which can generate income over time without constant effort.

Think of it like planting a tree. You nurture it in the beginning, but over time, it may grow and bear fruit with minimal intervention. However, just like any tree, it needs the right conditions to flourish, and there’s no guarantee of a bountiful harvest.

There are various ways to get started with passive investing:

- Index Funds: These funds track a specific market index, like the S&P 500, providing broad market exposure with low fees.

- ETFs (Exchange-Traded Funds): Similar to index funds, ETFs offer diversification and are traded on stock exchanges.

- REITs (Real Estate Investment Trusts): REITs allow you to invest in real estate without having to buy or manage properties directly.

It’s important to remember that all investments carry inherent risks, and diversification is key to managing those risks. For example, the S&P 500 has historically experienced an average annual volatility of around 15%, meaning that returns can fluctuate significantly year to year.

Investment Risk-Return Matrix

| Risk Level | Investment Type | Characteristics | Potential Return |

|---|---|---|---|

| Low Risk | Cash/Money Market | Highly liquid, very low-risk cash equivalents | 1-2% |

| CDs | Fixed-term deposits with guaranteed returns | 2-3% | |

| Government Bonds | Low-risk, government-backed securities | 2-4% | |

| Medium Risk | Corporate Bonds | Medium-risk debt instruments from companies | 4-6% |

| Gold | Traditional hedge against inflation | 5-7% | |

| S&P 500 Index | Broad market index of 500 large US companies | 7-10% | |

| High Risk | Real Estate | Property investments through REITs or direct ownership | 8-12% |

| Small-cap Stocks | Shares of smaller growth companies | 10-15% | |

| Cryptocurrency | Highly volatile digital assets | Highly Variable |

* This visualization is for illustrative purposes only. Actual risk and return levels may vary significantly.

* Historical returns and risk levels are based on general market observations and can change over time.

3. Owning Businesses: Taking Control (and Calculated Risks)

Many ultra-rich individuals own businesses. This allows them to control their income and make strategic decisions that can boost their wealth.

Think of it like being the captain of your own ship. You chart the course, navigate challenges, and reap the rewards of your efforts. But just like any captain, you face storms, rough seas, and the possibility of going off course.

Entrepreneurship comes with its own set of responsibilities and risks. Understanding different business structures, like sole proprietorships, LLCs, and S corporations, is crucial for tax planning and liability management.

4. Smart Borrowing: Using Leverage Wisely

While most people try to avoid debt, the ultra-rich sometimes use it strategically. They borrow money to invest in assets that are likely to appreciate in value, such as businesses or real estate. This is called leverage.

Think of it like using a lever to lift a heavy object. With the right leverage, you can achieve more with less effort. But be careful – too much leverage can make things unstable and lead to bigger problems.

It’s crucial to distinguish between good debt and bad debt. Good debt is used to invest in appreciating assets, while bad debt is used for consumption or depreciating assets. And always remember that borrowing involves risks, such as interest rate fluctuations and the potential for increased losses if your investments don’t perform as expected.

Think Like the Ultra-Rich: Cultivating the Right Mindset

- Long-Term Vision: They don’t chase get-rich-quick schemes. They focus on making decisions that will benefit them for years to come.

- Strategic Leverage: They seek opportunities that have the potential to multiply their money many times over, but they understand and manage the associated risks.

- Calculated Risks: They’re not afraid to take risks, but they always carefully consider the potential rewards and downsides before making a move.

- Independent Thinking: They don’t blindly follow the crowd. They conduct their own research and make informed decisions.

Building a Strong Financial Foundation: Emergency Funds and Debt Management

- Emergency Fund: Having 3-6 months of living expenses saved can provide a safety net in case of unexpected events like job loss or medical emergencies.

- Debt Management: Managing debt responsibly is crucial. Prioritize paying down high-interest debt and avoid unnecessary borrowing.

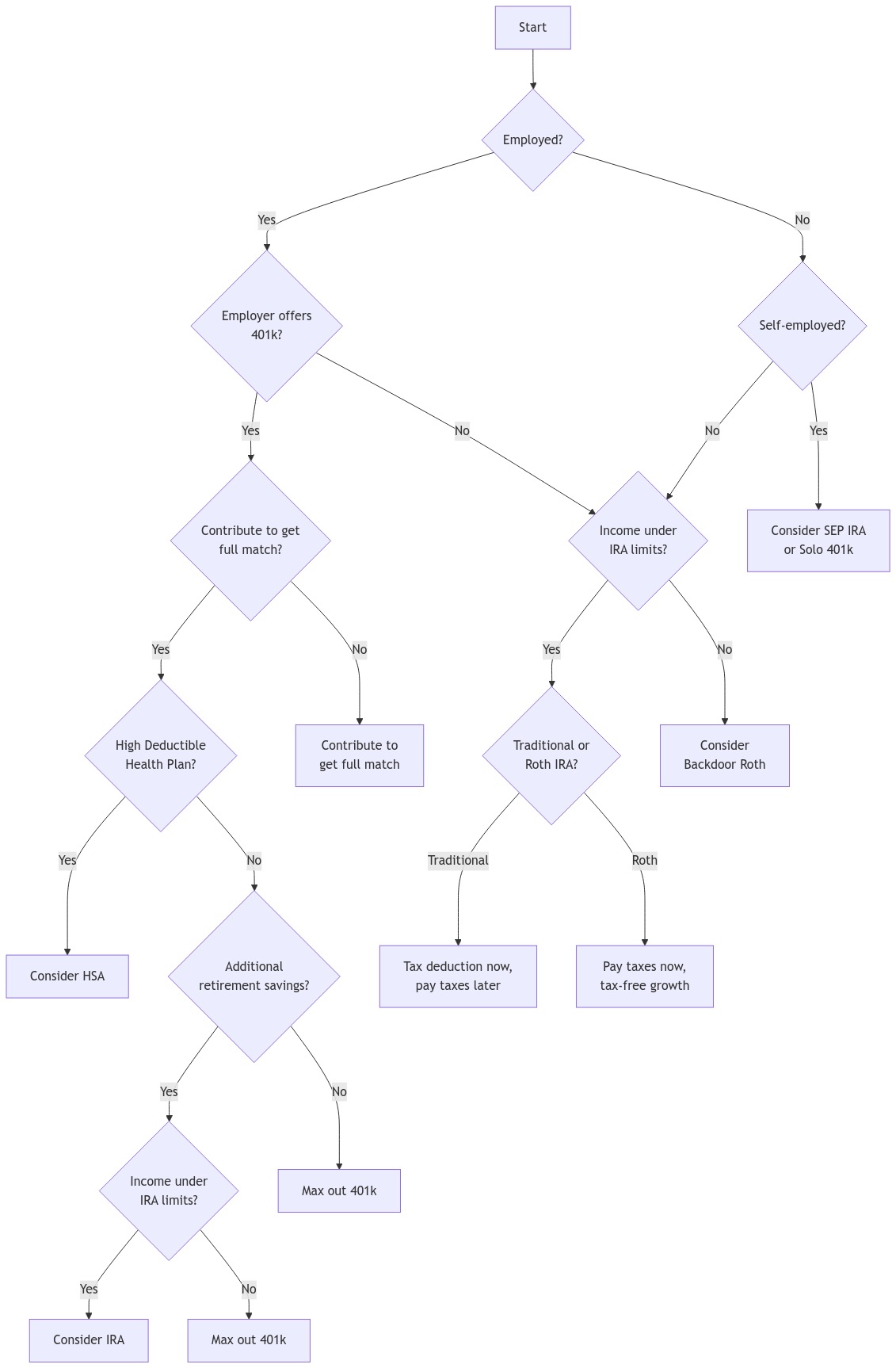

Tax-Advantaged Investing: Optimizing Your Returns

The ultra-rich understand the importance of minimizing their tax burden. Tax-advantaged accounts, like 401(k)s, IRAs, and HSAs, offer significant tax benefits that can accelerate wealth accumulation.

- 401(k)s: These employer-sponsored plans allow you to contribute pre-tax dollars, reducing your taxable income and allowing your investments to grow tax-deferred.

- IRAs (Individual Retirement Accounts): IRAs offer tax advantages for retirement savings, with different types like Traditional and Roth IRAs catering to various needs.

- HSAs (Health Savings Accounts): HSAs combine tax-free contributions and withdrawals with potential investment growth, making them a powerful tool for healthcare expenses.

At XOA TAX, our team of Certified Public Accountants (CPAs) can help you navigate the complexities of these accounts and develop a tax-efficient strategy as part of your overall financial plan.

FAQs

How can I start investing with limited funds?

Many investment platforms allow you to start with small amounts. Consider fractional shares or micro-investing apps to begin your investment journey.

What’s the best way to learn about investing?

There are numerous resources available, including books, online courses, and financial websites. It’s also helpful to seek guidance from experienced professionals, like a Certified Financial Planner.

How can I avoid making emotional investment decisions?

Develop a clear investment plan based on your risk tolerance and financial goals, and stick to it. Avoid making impulsive decisions based on market fluctuations or short-term trends.

Regulatory Compliance and Fiduciary Responsibility

At XOA TAX, our CPAs meet all state licensing requirements and adhere to the highest professional standards. You can verify our credentials by visiting the CPAVerify. We are committed to providing transparent and ethical services, which includes:

- Clearly Defined Scope: We focus on tax preparation, tax planning, and providing general financial guidance. We do not provide investment advice.

- Separation of Services: We maintain a clear distinction between tax services and investment advice. For investment recommendations, we encourage you to consult with a qualified financial advisor.

- State Compliance: We adhere to all applicable state regulations and ethical guidelines.

Connecting with XOA TAX

Planning for your financial future can be exciting, but it also requires careful consideration. If you’re feeling overwhelmed or unsure about where to start, XOA TAX can help. Our team of experienced CPAs can provide professional guidance and support to help you achieve your financial goals.

We can assist you with:

- Developing a comprehensive financial plan

- Understanding the tax implications of your investments

- Minimizing your tax burden through proactive tax planning

- Navigating complex financial decisions

We encourage you to verify our credentials and contact information independently.

Website: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/

Phone: +1 (714) 594-6986

Email: [email protected]

Contact Page: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/contact-us/

Disclaimer: This post is for informational purposes only and does not provide personalized legal, tax, or financial advice. Laws, regulations, and tax rates can change often and vary significantly by state and locality. This communication is not intended to be a solicitation, and XOA TAX does not provide legal advice. XOA TAX does not assume any obligation to update or revise the information to reflect changes in laws, regulations, or other factors. For further guidance, refer to IRS Circular 230. Please consult with a qualified professional advisor for advice specific to your situation.