The United States welcomes thousands of Canadian students each year, many of whom arrive on F-1 student visas to pursue their academic dreams. While navigating a new education system and culture can be exciting, it’s essential to understand your tax responsibilities. This guide will help Canadian students on F-1 visas understand their tax obligations in the U.S., including those related to income from work practicums and investments.

Key Takeaways

- Canadian students on F-1 visas are generally considered non-resident aliens for U.S. tax purposes.

- You may be required to file a U.S. tax return even if you have no income.

- The U.S. and Canada have a tax treaty that can help you avoid double taxation.

- Understanding your tax obligations is crucial for maintaining your visa status and avoiding penalties.

Understanding Your Tax Status

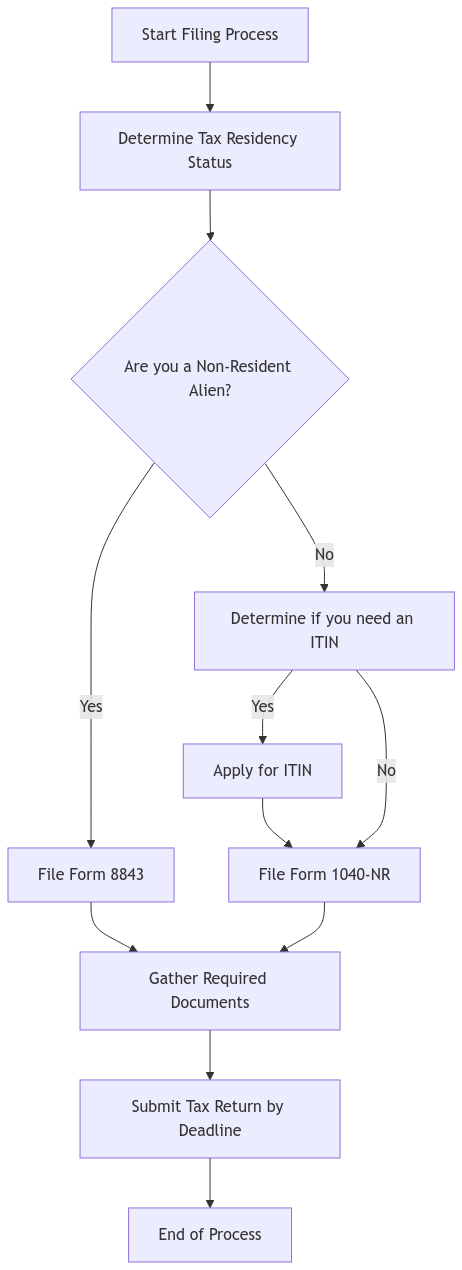

As a Canadian student on an F-1 visa, the U.S. Internal Revenue Service (IRS) generally considers you a non-resident alien for tax purposes. This means you are taxed differently than U.S. citizens or resident aliens. However, the duration of your stay and the substantial presence test can influence your residency status for tax purposes.

What is the Substantial Presence Test?

To determine if you meet the substantial presence test, the IRS looks at the current year and the two preceding years. You are considered a resident alien if you were physically present in the U.S. for:

- 31 days during the current year, and: 183 days during the three-year period, using a weighted formula: each day in the previous year counts as 1/3 of a day, and each day in the year before that counts as 1/6 of a day.

(Insert infographic here illustrating the substantial presence test. Alt text: Infographic explaining the substantial presence test for determining residency status in the U.S.)

The 5-Year Exemption for F-1 Students

For the first five calendar years as an F-1 student, you are exempt from the substantial presence test. This means that even if you meet the day count requirements, you are still generally considered a non-resident alien for tax purposes during this initial period.

Income Subject to U.S. Taxation

While specific rules apply, here are the common types of income Canadian students on F-1 visas may need to report:

- Wages from CPT and OPT Employment: Income earned through Curricular Practical Training (CPT) or Optional Practical Training (OPT) is generally considered U.S.-source income and subject to taxation. You will need to complete Form W-4, Employee’s Withholding Certificate, so your employer can withhold the correct amount of federal income tax from your wages. The standard withholding rate for non-resident aliens is 30%, but this can be reduced under the U.S.-Canada tax treaty.

- Scholarships and Fellowships: While some scholarships and fellowships may be tax-exempt, others are taxable. It’s essential to determine the taxable portion of any financial aid you receive. This information will be reported to you on Form 1042-S, Foreign Person’s U.S. Source Income Subject to Withholding.

- Investment Income: Interest and dividends earned on U.S. investments may also be taxable. You may need to complete Form W-8BEN, Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting, to claim treaty benefits and reduce or eliminate tax withholding on this income.

Tax Treaty Benefits

The U.S. and Canada have a tax treaty to prevent double taxation. This treaty can provide exemptions or reduced tax rates on certain types of income. For instance, under Article XX of the treaty, you might be eligible for a tax exemption on scholarship income.

Filing Your U.S. Tax Return

Even if you have no income, you are still required to file Form 8843, “Statement for Exempt Individuals and Individuals With a Medical Condition.” If you have taxable income, you’ll generally file Form 1040-NR, “U.S. Nonresident Alien Income Tax Return.” If you do not have a Social Security Number (SSN), you will need to apply for an Individual Taxpayer Identification Number (ITIN) to file your tax return.

Important Filing Deadlines:

- April 15th: The usual deadline for filing federal income tax returns.

- June 15th: Automatic extension to file your tax return if you are a nonresident alien who has not earned wages subject to U.S. income tax withholding.

Need help with your tax return? XOA TAX can assist you with navigating the complexities of filing as a non-resident alien. Contact us today!

It’s always best to file your tax return on time to avoid penalties. You can find detailed instructions and forms on the IRS website here. Keep in mind that some tax software programs have limitations for nonresident aliens, so you may need to explore specialized software or seek assistance from a tax professional.

Social Security and Medicare Taxes

As an F-1 student on a non-immigrant visa, you are generally exempt from paying Social Security and Medicare taxes on your wages. However, this exemption may not apply if you change your visa status or become a resident alien for tax purposes.

State Tax Obligations

In addition to federal taxes, you might also have filing requirements in the state where you reside and study. State tax laws vary, so it’s important to research the specific requirements for your state.

For example, if you are studying in California, you can find information about state tax obligations for nonresidents here.

Record-Keeping Checklist

Maintaining accurate records is essential for meeting your tax obligations. Keep these documents for at least three years.

Note: It’s recommended to keep tax records for at least three years. Consult with a tax professional for specific guidance.

Estimated Tax Payments

While most F-1 students will have taxes withheld from their wages, you might need to make estimated tax payments if you have other sources of income, such as investment income or taxable scholarships, that are not subject to withholding. Estimated taxes are paid quarterly to the IRS.

| Payment Period | Deadline |

|---|---|

| January 1 to March 31 | April 15 |

| April 1 to May 31 | June 15 |

| June 1 to August 31 | September 15 |

| September 1 to December 31 | January 15 of next year |

Note: If any of these deadlines fall on a weekend or holiday, the deadline is shifted to the next business day.

Remote Work and Internships

The tax implications of remote work and internships can be complex for F-1 students. If you are working remotely for a company outside the U.S. while physically present in the U.S., you may still be considered to have U.S.-source income. It’s essential to consult with a tax professional to understand your obligations in these situations.

FAQs

I only worked a part-time job on campus. Do I still need to file a tax return?

Possibly. Even if your income was low, you might still need to file a tax return. It’s best to review the IRS guidelines or consult with a tax professional to determine your specific requirements.

How can I get help with my tax return if I’m not sure what to do?

You can find helpful resources on the IRS website or seek assistance from a qualified tax professional specializing in international student taxation.

What happens if I don’t file my tax return?

Failing to file your tax return can result in penalties, interest accrual on any unpaid taxes, and potential issues with your visa status.

Don’t Let Taxes Stress You Out!

Navigating the U.S. tax system as a Canadian student can feel overwhelming. But it doesn’t have to be! XOA TAX is here to help. Our experienced CPAs specialize in international student taxation and can provide the guidance you need to stay compliant and minimize your tax liability.

We understand the unique challenges faced by international students. Our personalized approach ensures you receive the specific advice and support you need to navigate the U.S. tax system with confidence.

Contact us today for a consultation:

Website: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/

Phone: +1 (714) 594-6986

Email: [email protected]

Contact Page: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/contact-us/

Disclaimer: This post is for informational purposes only and does not provide legal, tax, or financial advice. Laws, regulations, and tax rates can change often and vary significantly by state and locality. This communication is not intended to be a solicitation, and XOA TAX does not provide legal advice. XOA TAX does not assume any obligation to update or revise the information to reflect changes in laws, regulations, or other factors. For further guidance, refer to IRS Circular 230. Please consult a professional advisor for advice specific to your situation.