Transferring assets from a joint brokerage account to an individual account is a common strategy used in estate planning, gifting, or simply managing personal finances. However, it’s important to be aware of the potential tax consequences before making any changes. This article will guide you through the key tax considerations involved in transferring joint brokerage accounts to individual ownership.

Quick Reference

- 2024 Annual Gift Tax Exclusion: $18,000 per person ($36,000 for couples)

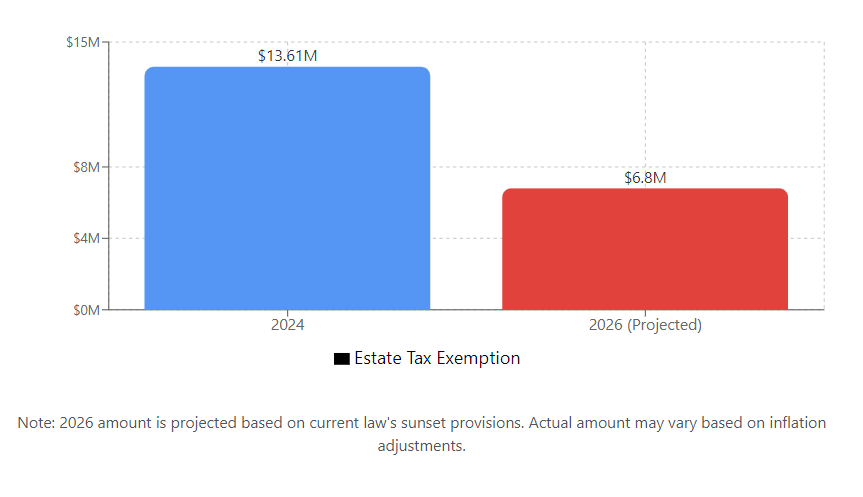

- Federal Estate Tax Exemption: $13.61 million (sunsets in 2025)

- Cost Basis: Recipients inherit the donor’s basis for gifted assets.

- State Rules: Vary significantly, with exemptions as low as $1 million.

- Required Filings: Form 709 for gifts exceeding the annual exclusion.

Gift Tax Considerations

When you transfer your share of a joint brokerage account to another person, such as a child or grandchild, the IRS may consider this a gift. Fortunately, the IRS allows you to gift a certain amount each year without incurring gift tax. In 2024, this annual gift tax exclusion is $18,000 per recipient, or $36,000 per recipient for married couples gifting together.

For example, let’s say a married couple wants to transfer $50,000 from their joint account to their daughter. They can each gift her $18,000 (totaling $36,000) without worrying about gift tax. The remaining $14,000 would count against their lifetime gift and estate tax exemption, which is $13.61 million per person in 2024.

If the value of the transferred assets exceeds the annual exclusion, you’ll need to file IRS Form 709 to report the gift. This helps track the use of your lifetime exemption.

Generation-Skipping Transfer Tax

If you plan to transfer assets to your grandchildren, be mindful of the generation-skipping transfer (GST) tax. This tax applies to gifts or bequests that “skip” a generation, such as gifts made directly to grandchildren. The GST tax has its own exemption amount, separate from the lifetime gift and estate tax exemption. In 2024, this exemption is also $13.61 million per individual.

Capital Gains Tax Implications

It’s crucial to understand the concept of “cost basis” when gifting assets. The cost basis is essentially the original price you paid for the asset, plus any adjustments for things like reinvested dividends and stock splits. When you gift an asset, the recipient generally inherits your cost basis.

This means that if the recipient sells the asset later, they may be liable for capital gains tax on any appreciation that occurred while you owned it. For instance, if you bought stock for $10,000 years ago, and now it’s worth $25,000, your cost basis is $10,000. If you gift that stock to your child, and they sell it for $25,000, they’ll be responsible for capital gains tax on the $15,000 gain.

However, if you were to bequeath the stock to your child through your will, they would receive a “step-up in basis” to the fair market value of the stock at the time of your death. In this case, their cost basis would be $25,000, and they would not owe any capital gains tax if they sold it immediately.

It’s important to note that special rules may apply to the calculation of cost basis for joint property in community property states.

Estate Tax Considerations

Federal Estate Tax

Transferring assets out of your estate can be a strategic way to reduce your taxable estate and potentially lower future estate tax liabilities. While the current federal estate tax exemption is quite high ($13.61 million per person in 2024), it’s important to remember that this exemption is scheduled to sunset after 2025, potentially dropping to around half the current amount.

Portability of the Federal Estate Tax Exemption

A key feature of the federal estate tax is the concept of “portability.” This allows a surviving spouse to use any unused portion of their deceased spouse’s estate tax exemption, effectively doubling the exemption amount for the surviving spouse.

State Estate Tax

Keep in mind that state estate tax rules can vary significantly. Some states have much lower exemption thresholds than the federal government.

Here’s a table comparing federal estate tax exemptions to those of some states with lower exemptions:

| Jurisdiction | 2024 Exemption Amount |

|---|---|

| Federal | $13.61 million |

| Oregon | $1 million |

| Massachusetts | $1 million |

| Washington | $2.193 million |

| District of Columbia | $4.845 million |

This table illustrates the wide variation in state estate tax exemptions. It’s crucial to consult with a tax professional to understand the specific rules in your state.

Reporting Requirements

Even if no gift tax is due because the value of your gift is below the annual exclusion, you may still need to file a gift tax return (IRS Form 709) if your gifts exceed the annual exclusion. This helps the IRS track the use of your lifetime exemption. Married couples who choose to “gift-split” must each file a separate Form 709, even though they are combining their annual exclusions for the gift. The deadline for filing Form 709 is the same as your income tax return, typically April 15th of the following year.

Failure to file required gift tax returns can result in penalties and complicate future estate planning.

Alternative Strategies

Gradual Gifting: To maximize the use of your annual gift tax exclusion, consider spreading gifts over multiple years. For example, instead of gifting $50,000 to your child all at once, you could gift $18,000 per year for three years.

Direct Payments: Payments made directly to a qualified educational institution for tuition or to a medical provider for medical expenses on behalf of someone else are not considered gifts and do not count against your annual exclusion. For example, if you pay your grandchild’s college tuition directly to the university, this would not be subject to gift tax. Similarly, if you pay your friend’s hospital bill directly to the hospital, this would not be considered a gift.

Establishing Trusts: Irrevocable trusts can be a powerful tool for removing assets from your taxable estate and providing greater control over how those assets are distributed. This can be particularly useful for larger estates or for individuals who want to ensure that their assets are used in a specific way.

Qualified Disclaimers: A qualified disclaimer allows a beneficiary to refuse a gift or inheritance. This can be a useful strategy if the beneficiary doesn’t need the asset or if accepting it would have negative tax consequences.

Basis Planning: For highly appreciated assets, consider strategies such as gifting appreciated stock to charity or using a grantor retained annuity trust (GRAT) to minimize capital gains tax.

State-Specific Considerations

It’s important to be aware that some states have their own gift tax rules, which may differ from federal regulations. For example, some states have lower annual exclusion amounts or impose a state gift tax even if no federal gift tax is due. Additionally, the rules for joint tenancy termination can vary by state.

Timing Considerations

The timing of asset transfers can also have tax implications. For example, if you anticipate that your income will be lower in a particular year, you may want to make larger gifts in that year to take advantage of lower tax brackets. Year-end planning is crucial for maximizing tax efficiency.

Stepped Transaction Doctrine

Be cautious of the “stepped transaction doctrine.” This doctrine allows the IRS to collapse a series of transactions into a single transaction if it appears that the transactions were planned and executed as part of a larger scheme to avoid taxes. For example, if you transfer assets to a trust and then immediately distribute those assets to a beneficiary, the IRS may view this as a direct gift from you to the beneficiary, subject to gift tax.

Timeline Example:

| Date | Action |

|---|---|

| January 1 | Create trust |

| January 2 | Transfer assets to trust |

| January 3 | Distribute to beneficiary |

IRS View: May be treated as a direct gift to the beneficiary.

Transfers to Non-U.S. Citizens

If you’re considering transferring assets to someone who is not a U.S. citizen, be aware that different rules apply. Gifts to non-U.S. citizens may be subject to different tax rates and reporting requirements.

Need Help Navigating the Complexities of Asset Transfers?

Transferring assets can be a complex process with significant tax implications. At XOA TAX, we’re here to help you understand your options and make informed decisions that align with your financial goals. Contact us today for personalized advice and guidance.

Website: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/

Phone: +1 (714) 594-6986

Email: [email protected]

Contact Page: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/contact-us/

Disclaimer: This post is for informational purposes only and does not provide legal, tax, or financial advice. Laws, regulations, and tax rates can change often and vary significantly by state and locality. This communication is not intended to be a solicitation, and XOA TAX does not provide legal advice. Please consult a professional advisor for advice specific to your situation.