Hey there, fellow taxpayers! It’s your Friendly Financial Coach from XOA TAX, here to help you navigate the sometimes confusing world of tax deductions. Today, we’ll tackle a common question that pops up as we approach the end of the year: Should you take the standard deduction or itemize?

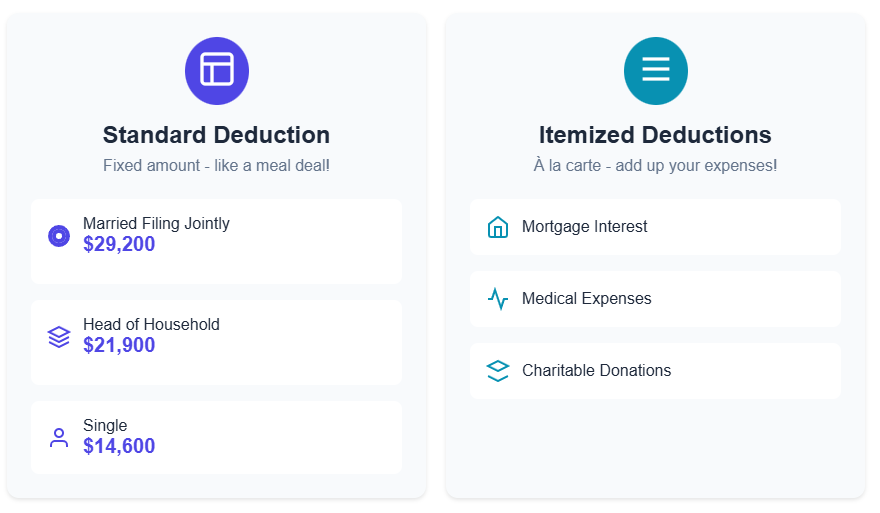

Think of it like choosing between a pre-set meal deal at your favorite restaurant or ordering à la carte. The standard deduction is like the meal deal – a fixed amount that reduces your taxable income. For 2024, it’s $29,200 for married couples filing jointly, $21,900 for heads of household, and $14,600 for single filers and married couples filing separately.

Bonus tip: If you’re 65 or older or happen to be blind, you get a slightly higher standard deduction!

Itemizing, on the other hand, is like ordering à la carte. You add up all your eligible expenses – things like mortgage interest, charitable donations, and medical expenses – and that total reduces your taxable income.

So, which option is best for you?

Well, it depends on which one gives you the biggest deduction! Let’s break it down with a few scenarios:

Scenario 1: The Homeowner

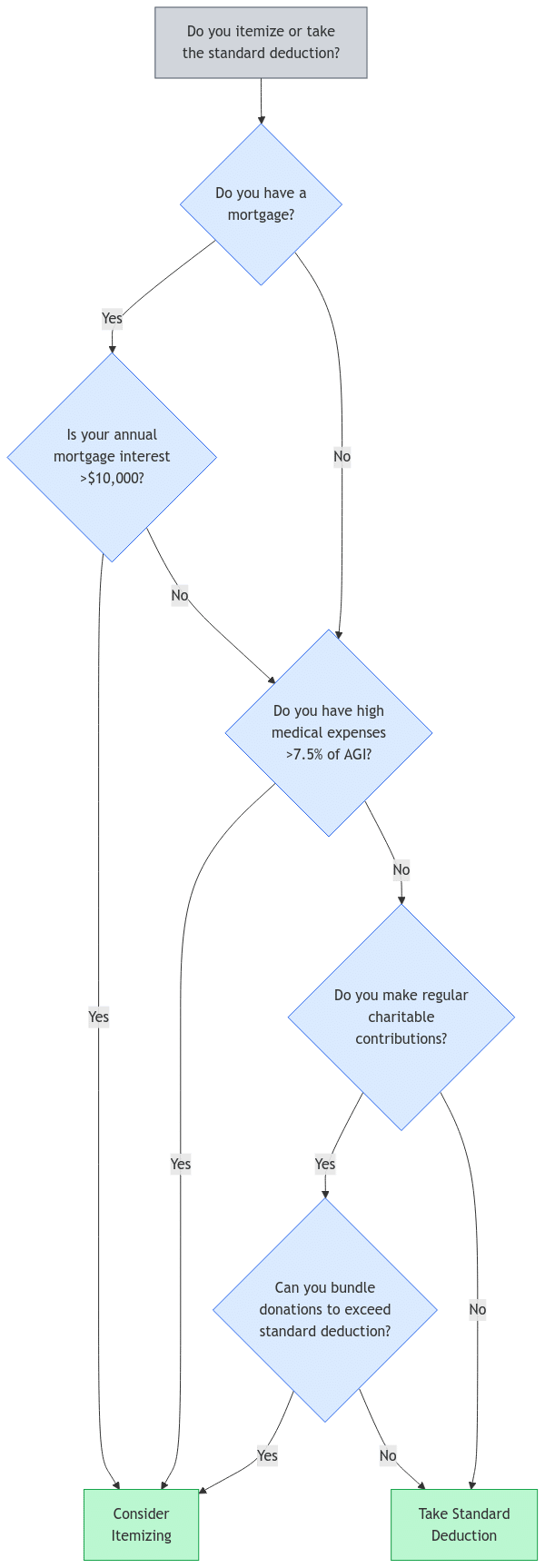

Imagine you’re a homeowner with a mortgage. By making your January mortgage payment in December, you can actually deduct the interest for 13 months instead of just 12 on your 2024 tax return. That’s an extra deduction that could push you past the standard deduction amount, saving you some serious cash!

Scenario 2: The Charitable Giver

Do you donate to charity regularly? Consider making a larger donation this year and a smaller one next year. This could boost your itemized deductions for 2024, especially if you’re already close to surpassing the standard deduction.

Scenario 3: The Medically Minded

If you’ve been putting off elective medical procedures, dental work, or vision care, and you think your medical expenses might exceed 7.5% of your adjusted gross income (AGI), you might want to schedule those appointments before the year ends. Remember, you can only deduct the amount exceeding that 7.5% threshold.

A Word of Caution: The SALT Limit and the AMT

While prepaying state and local taxes (like property taxes) might seem like a good idea, there’s a catch. You can only deduct up to $10,000 ($5,000 if married filing separately).

Also, watch out for the Alternative Minimum Tax (AMT)! It’s a different way of calculating your taxes, and it doesn’t allow deductions for state and local taxes. While fewer people are subject to the AMT since the Tax Cuts and Jobs Act, it’s still something to be aware of.

Feeling overwhelmed? Don’t worry, we’re here to help!

This is just a taste of the strategies you can use to minimize your tax bill. Every taxpayer’s situation is unique, so it’s always best to get personalized advice. The friendly experts at XOA TAX can help you crunch the numbers and determine the best approach for you.

FAQs

What if my itemized deductions are only slightly less than the standard deduction?

It might be worth looking for ways to increase your itemized deductions, such as those mentioned above. Even a small increase could make a difference!

Where can I find more information about what qualifies as an itemized deduction?

The IRS website is a great resource, or you can always reach out to us at XOA TAX. We’re happy to answer your questions.

Can I switch between taking the standard deduction and itemizing from year to year?

Absolutely! You have the flexibility to choose the option that benefits you most each year.

Connecting with XOA TAX

We hope this post has shed some light on the standard deduction vs. itemizing dilemma. Remember, we’re here to help you navigate the complexities of tax season and make the process as stress-free as possible.

Contact us today for personalized guidance and support!

Website: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/

Phone: +1 (714) 594-6986

Email: [email protected]

Contact Page: https://bwgv2xepn2kgo7imbfjg-production-sites.xoatax.net/contact-us/

Disclaimer: This post is for informational purposes only and does not provide legal, tax, or financial advice. Laws, regulations, and tax rates can change often and vary significantly by state and locality. This communication is not intended to be a solicitation, and XOA TAX does not provide legal advice. XOA TAX does not assume any obligation to update or revise the information to reflect changes in laws, regulations, or other factors. For further guidance, refer to IRS Circular 230. Please consult a professional advisor for advice specific to your situation.